Japanese Yen Talking Points

USD/JPY[1] slips to a fresh monthly-low (111.97) amid the recent rout in risk appetite, and the exchange rate may stage a larger correction over the remainder of the week as it extends the series of lower highs carried over from the previous week.

USD/JPY Rate Outlook Mired by Lower Highs, Lackluster U.S. CPI

The fresh updates to the U.S. Consumer Price Index (CPI) have done little to prop up USD/JPY as the headline reading narrows more-than-expected in September, with the figure slipping to 2.3% from 2.7% per annum the month prior.

A deeper look at the report showed the core rate of inflation also falling short of market expectations as the gauge held steady at 2.2% for the second consecutive month, and signs of easing price pressures may start to sway the outlook for monetary policy as the development highlights a limited threat for above-target inflation.

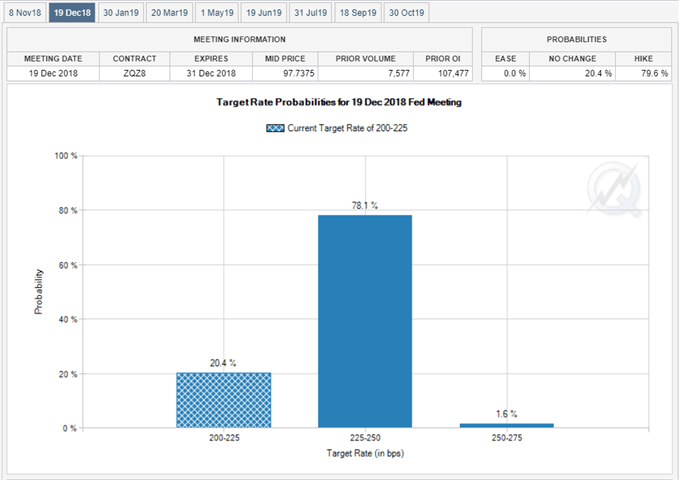

The recent batch of lackluster data prints may force the Federal Open Market Committee[2] (FOMC) to soften its hawkish tone especially as President Donald Trump warns that the ‘Fed is making a mistake,’ but it seems as though Chairman Jerome Powell & Co. have little to no interest in deviating from the hiking-cycle as the central bank largely achieves its dual mandate for full-employment and price stability.

With that said, Fed Fund Futures may continue to reflect expectations for another 25bp rate-hike at the next quarterly meeting in December, and the material shift in retail interest may continue to materialize over the near-term amid the pickup in market volatility.

The IG Client Sentiment Report[3] shows 38.8% of traders are net-long USD/JPY,